Here's how marriage and divorce will affect your Social Security benefits

Social Security benefits are a substantial source of income for many older adults. Among those age 65 and older, 37% of men and 42% of women rely on their checks for at least half of their income, according to data from the Social Security Administration.

Several factors will affect the size of your payments, including your income history, the length of your career, and the age you begin claiming. But your marital status will also have an impact on your benefit amount.

If you're married or divorced, you could be entitled to a special type of Social Security. The average retiree eligible for this type of benefit collects around $912 per month, as of January 2024, so it pays to see whether you qualify.

Who qualifies for spousal benefits?

Spousal benefits are a special type of Social Security reserved for married or divorced retirees. To qualify for spousal benefits as a married retiree, there are a few requirements you'll need to meet:

- You must currently be married.

- Your spouse must be eligible for Social Security retirement or disability benefits.

- You must be at least 62 years old — unless you're caring for a child who is either under age 16 or disabled, in which case this rule may not always apply.

If you're divorced, you could still qualify for extra Social Security through divorce benefits. The requirements for this type of benefit, though, are a little different:

- You cannot currently be married (though it's OK if your ex-spouse has remarried).

- Your previous marriage must have lasted for at least 10 years.

- If you've been divorced for less than two years, you'll need to wait until your ex-spouse begins taking Social Security before you can file for divorce benefits.

For both spousal and divorce benefits, your benefit will not affect how much your spouse or ex-spouse receives from Social Security. Also, if your ex-spouse has remarried, taking divorce benefits will not affect his or her current partner's ability to claim spousal benefits.

How much can you receive?

With both types of benefits, the maximum payment is 50% of the amount your spouse or ex-spouse is entitled to receive at his or her full retirement age (FRA). If you're also entitled to retirement benefits based on your own work history, the Social Security Administration will only pay out the higher of the two amounts — not both.

So, for example, say you qualify for $1,000 per month in retirement benefits at your FRA, while your spouse will receive $3,000 per month at his or her FRA. In this case, your spousal benefit would be $1,500 per month. Because that's higher than your retirement benefit, that's how much you'll receive each month — not $2,500 per month.

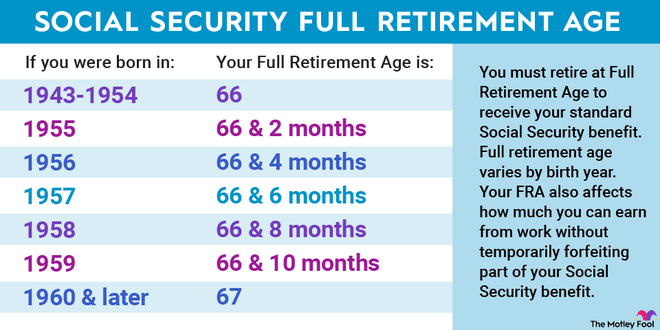

To receive the full amount you're entitled to in spousal or divorce benefits, you'll need to wait until your FRA to file. Your FRA will fall between ages 66 and 67, and if you begin claiming before that age, you'll receive reduced payments each month.

One exception to this is if you're caring for a child who is under age 16 or disabled. If you begin claiming before your FRA, your benefit generally will not be reduced.

Also, unlike standard retirement benefits, delaying claiming past your FRA won't increase your spousal or divorce benefit. And if your spouse or ex-spouse delays Social Security, that also won't boost your payments. In either case, the highest amount you can receive is 50% of your spouse's FRA benefit.

Social Security can go a long way in retirement, and spousal or divorce benefits could boost your checks by hundreds of dollars per month. By taking full advantage of every type of benefit you qualify for, you can set yourself up for a more financially secure retirement.

The Motley Fool has a disclosure policy.

The Motley Fool is a USA TODAY content partner offering financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

Offer from the Motley Fool:The $22,924 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Simply click here to discover how to learn more about these strategies.

View the "Social Security secrets"

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.