Student loan repayments will restart soon. What happens if you don't pay?

For more than three years, people with student loans haven't had to repay their debt, thanks to a pandemic-era break that is slated to come to an end in October, when repayments resume. But some borrowers say they aren't financially prepared to restart payments, while others may simply be unaware that repayments are due.

That raises the question of what happens to borrowers if they don't resume paying their loan balances in October. While the answer is complicated, many borrowers may be able to skip repaying their loans without serious consequences — at least for a while — experts say.

The reason? The Biden Administration is creating what it calls an "on-ramp" for student loan repayments that is aimed at easing the financial pain for the nation's 44 million borrowers. The on-ramp, announced on June 30 after the Supreme Court blocked President Joe Biden's student-debt forgiveness program, will give borrowers a one-year grace period for missed payments.

"It's critically necessary that we have some kind of, like, reprieve for borrowers because the reality is that most Americans' budgets don't have the flexibility to suddenly be making what is often hundreds of dollars of monthly payments right now," noted Persis Yu, deputy executive director at the advocacy group Student Borrower Protection Center.

Only 30% of borrowers know when their payments are slated to resume, while almost half said they aren't financially prepared to begin repaying their debt, according to a recent survey from U.S. News & World Report.

When do student loan repayments resume?

Interest will start accruing on September 1, and loan repayments will begin in October.

What is the "on-ramp" for student loans?

This is a one-year leniency program that will begin Oct. 1, 2023 and end on Sept. 30, 2024.

The program will "help borrowers avoid the harshest consequences of missed, partial or late payments," according to the Education Department.

Borrowers who miss or are late in their payments won't be reported to the credit reporting agencies, nor will they be considered in default. Their loans also won't be sent to collection agencies.

"It's basically going to be a forbearance that borrowers don't need to take action to get into," Yu noted.

Does that mean I can skip repaying my loans?

It depends on your tolerance for financial pain down the road. While the worst consequences of missing your loan payments will be waived until September 30, 2024, interest will continue to accumulate during the on-ramp period.

"People do need to know that they will continue to accrue interest — their balances will grow," Yu noted. "So if they're not making payments during this time, then their balance will be higher come September 2024."

Don't skip payments if you can get into the SAVE program

Skipping repayment may seem enticing, especially if you don't have the budget to start repayments, but there is another option that could provide even more help to millions of borrowers, experts say.

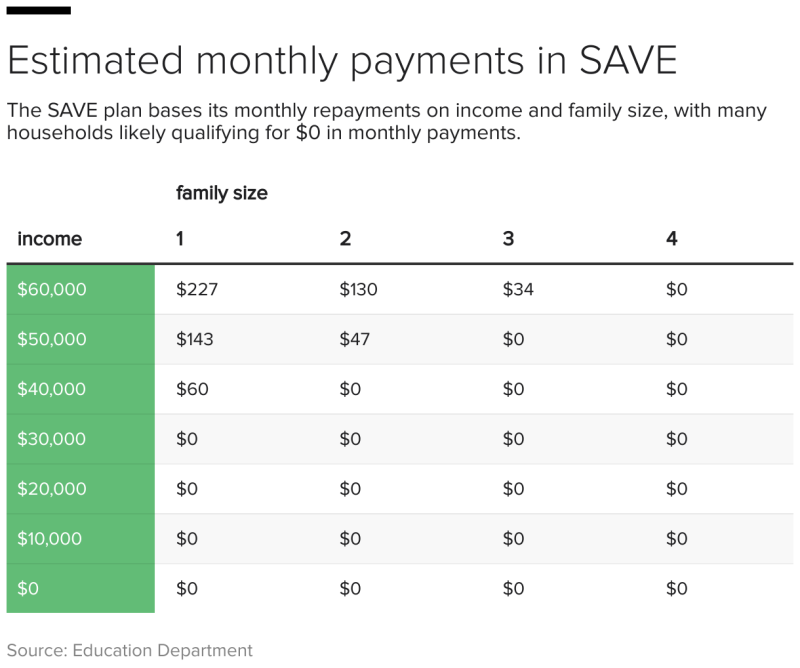

That option is the new Saving on a Valuable Education (SAVE) plan, an income-driven repayment program, or IDR, which pegs a borrower's monthly payment to their income.

The SAVE program, which opened this month through a beta application, could cut monthly payments in half or even to $0 for borrowers. Many will save up to $1,000 a year on repayments, according to the Biden administration.

For households whose monthly payments would be $0 under SAVE, it would make more sense to enroll in the program than to use the on-ramp, mostly because interest doesn't accrue on balances for people in the IDR program, Yu noted.

"With the on-ramp, they will accrue interest, but if they get into SAVE, they will not accrue interest and yet the impact on their monthly budgets will be the same," she added. "Understanding that dynamic is gonna be really, really important."

- In:

- Student Loan

- Student Loans

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.